by OpenWrks

The Open Banking Implementation Entity recently announced that the ecosystem reached two-million users.

At OpenWrks this announcement marks a huge milestone in the journey to Open Banking becoming part of people’s everyday lives. But is Open Banking going to reach adoption? In this

article we will revisit the past two and half years, exploring scalability, consumer demand and asking the question - has Open Banking moved past the tech and regulatory talk and into a phase where it is improving everyday lives?

Is anyone using Open Banking?

After formally launching at the start of 2018, initial consumer adoption of Open Banking was slow. For those close to the market this was not a surprise as the underlying technology that makes Open Banking possible required testing, iteration and scaling to support customers at volume. From this steady start, demand has grown exponentially over the past two years as more product providers, banks and FinTechs, known as Third Party Providers (TPPs), make services available which unlock the value of Open Banking for consumers. With over 250 businesses now authorised to provide Open Banking services consumers and small businesses are being presented with more opportunities to use Open Banking to better understand their finances and move money easily. Authorised TPPs are now making over 500 million (534.6 million successful API calls) API calls every month - a whopping 383.8% growth year on year.

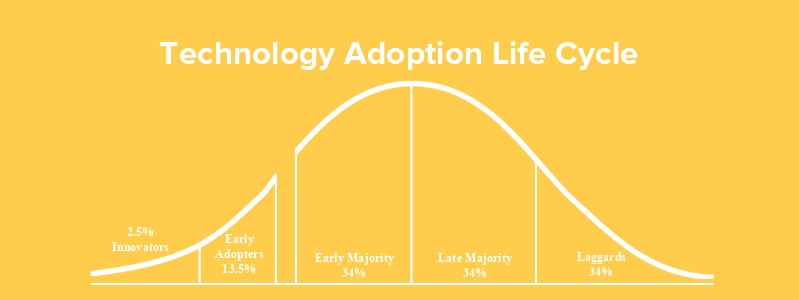

With 2 million people using Open Banking we have entered the crucial early adopter stage of the technology adoption lifecycle, as people using Open Banking move beyond the Innovators (those that have to try the latest “stuff”) into those people who whilst early to the party require the same value exchange to use a service.

This level of adoption suggests TPPs have discovered the first use cases that deliver enough value to the user in exchange for them consenting to share their financial information. The use cases achieving this include:

- Viewing all my bank accounts in one app

- Automating Income & Expenditure assessments

- Tracking spending against a target budget

- Identifying opportunities to switch providers on key bills

- Small businesses viewing their real-time bank balance alongside their invoices and management accounts

- Making bank to bank payments

To engage the early majority and see mass adoption of Open Banking, these use cases need to be made accessible and available to more consumers, more frequently.

Accessibility today - As more banks make APIs available for more account types e.g. Monzo, Starling, American Express, and Sainsbury’s Bank, more people can use Open Banking when it is made available to them - it’s estimated that the ecosystem now covers 99% of the addressable online banked market.

Availability today - As more companies make Open Banking powered products available - such as OpenWrks partners including, Lowell, Nationwide and HSBC - more consumers will come across it more often in all aspects of managing their money, increasing its familiarity and increasing people’s confidence and trust.

Another factor is likely to accelerate adoption as companies might soon find that they have no choice but to make services using Open Banking available to their customers, as regulators mandate that companies evidence consumers' affordability to borrow.

So the ecosystem is scaling… but what do consumers want from Open Banking?

Consumers don’t actively seek out Open Banking, instead they use it as a means to get value or a service which will improve their lives.

For example, a couple are looking to buy their first home so visit a mortgage adviser to help them work out what they can afford. The mortgage adviser gives them two options ahead of their appointment:

- To gather all of their bank statements, payslips and existing debt amounts and to go over them in detail in the appointment, which will increase their time with the adviser to an hour

- Or, they’re offered to complete a digital income and expenditure in their own time, in and around work, before their appointment, giving them anonymity and reducing the appointment time by half

The couple chooses to complete a digital Income and Expenditure and consent to the use of Open Banking as it will:

- save them time,

- reduce stress, as they don’t have to sit through what feels like an interrogation of their finances with their adviser,

- and give them an outcome which they can trust and confirm is accurate.

Without providing greater transparency and convenience consumers won’t consent to the use of Open Banking. It’s up to us and TPPs across the ecosystem to provide products which unlock this value for consumers.

How does Lowell use Open Banking?

As one of the first in the industry to make the benefits of Open Banking available to its customers, Lowell enables customers who are struggling to afford their payments to build a household budget so they understand what they can afford to repay. By using OpenWrks’ MyBudget tool Lowell offers its customers a transparent and convenient way to work out what they can repay in their own time and at their own pace.

Lowell is leading the way by using Open Banking to help people who are struggling financially, a segment of consumers often overlooked by digital innovations. Working collaboratively and gathering direct customer feedback, Lowell and OpenWrks are continuously iterating the user experience to ensure that the value of Open Banking is maximised to help every customer get the appropriate outcome that helps them repay their debts.

Alongside OpenWrks, Lowell continues to offer its manual budget calculator, and phone calls with customer service agents, for those without online banking capability and those who prefer not to use Open Banking.

How do Lowell’s customers complete an Open Banking powered budget?

It’s quick and easy to build a budget with OpenWrks MyBudget and only takes three simple steps:

- Step One, Create a MyBudget account

This allows customers to save their progress and complete their budget in and around their everyday lives. - Step Two, Connect their accounts using Open Banking

Customers then connect their accounts, this allows MyBudget to categorise transactional payments and automatically sort income and spending into groups. - Step Three, Finish the budget

MyBudget asks customers to confirm their income, identify any missed spending - for example, if a regular bill is paid out of an unconnected account - and finally asks them to confirm that their budget is correct.

MyBudget gives customers sight of their budget, the ability to confirm that it’s correct, and remove spending or income which is no longer received.

By empowering customers to build their own budget, it not only helps Lowell understand what they can realistically afford each month, but also helps them understand where they’re overspending and how much they have leftover to cover their debts.

Danielle Oxley, Customer Experience Centre Operations Manager at Lowell added: “It’s early days for Open Banking and as an industry and business we’re learning each and every day how to improve customer experience and provide real value. Two years after inception with two million users, is no mean feat. However, the industry can’t rest on its laurels, it needs to continue to explore the benefits that Open Banking can provide to people’s everyday lives, to ensure it continues to encourage more customer adoption.”

So is Open Banking improving everyday lives yet?

If you want to make sure each customer is getting an accurate, affordable, and sustainable outcome, Open Banking provides a transparent and convenient way for customers to understand what they can afford and agree repayments that work for them.

As the ecosystem continues to scale, in turn more consumers get exposed to Open Banking in their everyday lives. The rapid scale over the past six months puts the industry in a confident position to reach the early majority and help more people understand what they can afford to save, invest, borrow and repay.

If you’d like to find out more about how OpenWrks are using Open Banking to help people understand what they can afford take a look at our website.